Market Report

The Future of Spunlace Nonwovens to 2026

The elevated consumption of disinfecting wipes due to COVID-19, and plastics-free demand from governments and consumers and growth in industrial wipes are creating high demand for spunlace nonwoven materials through 2026, according to new research from Smithers. The report by veteran Smithers author Phil Mango, The Future of Spunlace Nonwovens through 2026, sees increasing global demand for sustainable nonwovens, of which spunlace is a major contributor.

The largest end use for spunlace nonwovens by far is wipes; the pandemic-related surge in disinfecting wipes even increased this. In 2021, wipes account for 64.7% of all spunlace consumption in tonnes. The global consumption of spunlace nonwovens in 2021 is 1.6 million tonnes or 39.6 billion m2, valued at $7.8 billion. Growth rates for 2021–26 are forecast at 9.1% (tonnes), 8.1% (m2), and 9.1% ($), the Smithers’ study outlines. The most common type of spunlace is the standard card-card spunlace, which is 2021 accounts for about 76.0% of all spunlace volume consumed.

Spunlace in wipes

Wipes are already the major end-use for spunlace, and spunlace is the major nonwoven used in wipes. The global drive to reduce/eliminate plastics in wipes has spawned several new spunlace variants by 2021; this will continue to keep spunlace the dominant nonwoven for wipes through 2026. By 2026, wipes will grow its share of spunlace nonwovens consumption to 65.6%.

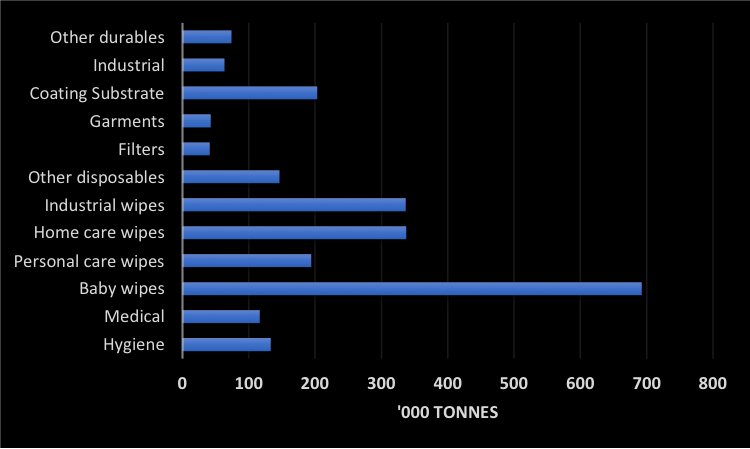

Spunlace nonwovens consumption by end-use, 2026 (tonnes)

Source: Smithers

Source: Smithers

COVID-19

COVID-19 has been a short-term, intense market driver that has had its primary effect in 2020-21. Most spunlace containing disposable products either saw significant increases in demand due to COVID-19 (for example, disinfecting wipes) or at least normal to slightly higher demand (for example, baby wipes, feminine hygiene components).

The years 2020-21 are not stable years for spunlace. Demand is recovering from significant surges in 2020 and early 2021 to a “correction” in demand in late 2021-22, back to more historical rates. The year 2020 saw margins well above the maximum average margin of 25% for some products and regions, while late 2021 is experiencing margins near the lower end of the range as end users work off bloated inventories. The years 2022-26 should see margins return to more normal rates.

Sustainability and plastic-free products

One of the most significant drivers of the last decade is the drive to reduce/eliminate plastics in wipes and other nonwoven products. While the European Union’s single use plastics directive was the catalyst, the reduction of plastics in nonwovens has become a global driver and especially for spunlace nonwovens.

Spunlace producers are working to develop more sustainable options to replace polypropylene, especially spunbond polypropylene in SP spunlace. Here, PLA and PHA, though both “plastics” are under evaluation. PHAs especially, being biodegradable even in marine environments, may be useful in the future. It appears the global demand for more sustainable products will accelerate through 2026.

Flushability

Multiple standards for flushable nonwovens have now been developed with the nonwoven and wastewater industries agreeing on the contents of GD4, IWGFS, Safe2Flush. The INDA/EDANA Guidance Document for Assessing the Flushability of Nonwoven Disposable Products, Fourth Edition (abbreviated as GD4) has become more rigorous in trying to develop testing which will accurately simulate a wipe's behavior in various wastewater treatment systems, including septic tank systems and low lying geographical regions systems (for example, the Netherlands in Europe, New Orleans in the US). Most flushable wipes products in 2021 have undergone repeated testing and are qualified as compliant.

Flushability is not a major desire for baby wipes; they are not primarily used near a toilet and typically are disposed of with the diaper. INDA/EDANA are concerned that if some baby wipes are marketed as flushable, the consumer may flush non-flushable baby wipes. Still, plastics-free baby wipes are of interest and spunlace variants like WLS, CP wet, and HEA are all useful in this market. Standard card/card (CC) spunlace using all non-plastics fibres are also candidates.

Industrial wipes

Some applications of industrial wipes include automobile body degreasing, printing press cleaning, cooking grill cleaning, clean room wipes, polishing, skin preparation, antibacterial and patient preparation. These products are almost all card/card (CC) or card/pulp/card (CPC) spunlace, polyester, rayon, polypropylene and wood pulp. Industrial wipes include products for general use, specialty, food service and healthcare. The fundamental drivers for industrial wipes are cost and performance.

Due to COVID-19, food service wipes were almost completely shut down in 2020 (along with restaurants, cafeterias and schools). General purpose wipes were also seriously affected, as janitorial services and most businesses were also closed. Wipes used in healthcare grew at above normal levels as hospitals and related facilities operated at near capacity. Some segments may take years to recover in some regions, but projections are for near normal levels of use by 2022.