Regardless of setbacks related to COVID-19 and associated large-scale disruptions in economic activity and transportation, fleet tire consumption is being bolstered by rebounding GDP performance, population and middle class expansion, and the emergence of new vehicle operation and ownership modes over the next five years. Greater efficiencies in commercial transport and the emergence of car and ride sharing fleets in personal transportation are driving growth in the fleet tire market, according to a new report from Smithers,

The Future of Fleet Tires to 2026.

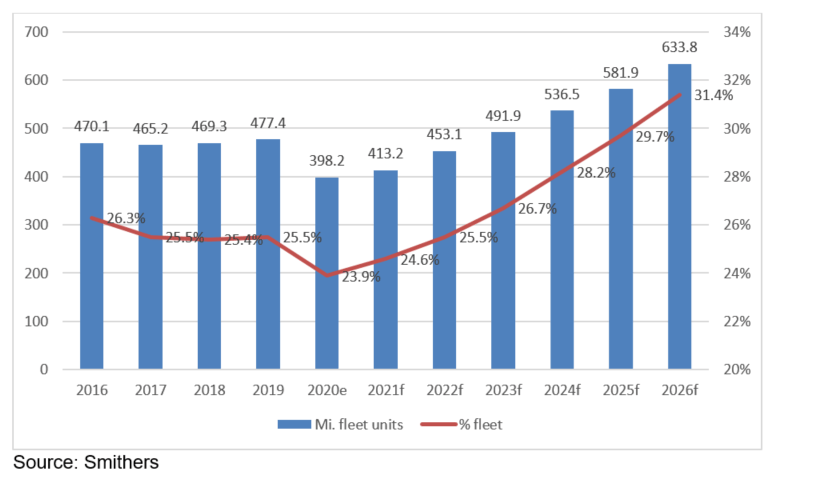

Demand from the fleet channel for light vehicle and truck and bus tires is estimated at $64.6 billion in 2021 and is expected to outpace the overall tire market in its recovery from the COVID-19 downturn, growing 8.7 percent per year through 2026. In unit terms, this translates to over 413 million units in 2021 and nearly 634 million in 2026, with an annual growth rate of 8.9 percent, decisively faster than the overall tire market.

Global fleet tire market and share of total tire market, 2016-26, by volume (million units/% share

The very attractive fleet tire growth rate is the product of an overall rebound from a still-low base year in 2021, and of a rebound in the rate of fleet penetration, first returning to its historical range by 2023, and then rising further as mobility trends, vehicle technology and scale economies of larger fleets begin to transform the composition of vehicle and tire markets ahead of the confluence of autonomous, shared fleets beyond the forecast period.

The Impact of COVID-19

The fleet tire market is supported by a wide variety of factors, most of which have been positive for most product and regional market segments until early 2020, when the COVID-19 virus emerged. The sweeping economic and mobility restrictions intended to mitigate its spread, were adopted by national, regional and local governments around the world.

The COVID-19 pandemic, and the closures and restrictions that many governments adopted to various degrees, set back the economy, vehicle sales and usage, and fleet vehicle sales, use, tire wear and tire replacement. In addition to reductions in economic activity, employment and commuting, shared transportation (e.g., taxis, buses, ride sharing) was scaled back. Fleets deferred new vehicle purchases in many areas. But there were also opportunities revealed, such as via the growth of e-commerce and delivery vehicles, which will help shape the fleet tire market for years to come.

COVID-19 also caused a pullback in the massive investments that had been flowing into electric and autonomous vehicle and tire development, shifting the uptake curves of these technologies out perhaps two years. We see these trends resuming to help expand the fleet market as recovery takes hold around the middle of the forecast period and to support broader transformation of mobility and tire markets beyond that, to a fleet-dominated shared, autonomous future.

New technology investment

Technology has been the target of increasing investment for years, and despite the delays encountered due to COVID-19 and related matters, it will continue to be the focus of major auto and tire companies. Connected, electric and autonomous shared transport are not only future concepts, they are strategic imperatives for automakers, tire manufacturers and their suppliers, tech firms and governments.

Tires will need to join rest of vehicle in connectivity through sensors or other systems providing real-time data on tire inflation, condition and wear. Increasingly, required for reasons of emissions and sustainability, growth of electric vehicles will be driven by political and regulatory imperatives and mandates. The advantage will go to those fleets that can more readily afford EVs and the needed charging infrastructure. Development of autonomous vehicles, which is being driven by safety and (when shared) congestion reduction and vehicle utilization optimization, will transform passenger mobility and much of commercial transport, particularly in urban areas.

The confluence of these new automotive technologies, on top of the current fleet paradigm, support the vision of corporate and government planners for a global vehicle parc characterized by connected, electric, autonomous and shared (or fleet-owned and operated) vehicles for passenger and commercial mobility and logistics.

Increasing light-vehicle demand

In value terms medium and heavy-duty trucks (and buses) dominate the fleet tire market at roughly twice the size of light vehicles (passenger cars in light trucks). Although in volume terms, light vehicles (a strong fleet market already mostly in Europe) dominate. Light-vehicle demand is experiencing higher growth, as ownership begins to migrate more towards fleets, which have been common in the more mature truck segment for many years already. But significant opportunities are seen in truck segments such as last-mile delivery, which has received a major long-term boost from changes brought about by COVID-19 and e-commerce. In general, smaller vehicles will be growing the fastest within their relevant segments.