Demand for flexible packaging (paper, foil and plastics) will reach a total of $248.6 billion in 2021, according to the latest exclusive research from Smithers, in its new report

The Future of Global Flexible Packaging to 2026.

This represents a moderate rise on 2020, a year where market growth was affected adversely by the Covid-19 pandemic, especially for industrial flexible formats. The prospects of a recovery, already evident in Asia, and spreading into North America and Europe as the Covid threat recedes leads Smithers to forecast global market growth at a compound annual growth rate (CAGR) of 3.2%. This will see total global value reach $294.1 billion in 2026.

Across the same period total tonnage of consumer flexible format packaging used will rise from 32.22 million tonnes to 39.54 million tonnes.

Geographic perspectives

As it evolves the majority of future growth will come from Asia-Pacific. The region is forecast to have a 5.4% CAGR for the next five years. Growth will be slowest in Western Europe, followed by Latin and North America.

Western Europe is a largely saturated market, and one where there is mounting pressure to substitute away from hard to recycle plastics in many key applications. The first deadline for the Single-use plastics Directive will pass in July 2021, including a ban on oxo-degradable plastics. Further restrictions on plastics are likely in Europe and beyond, over the next decade. In some applications a substitution to a new generation of flexible paper packaging is becoming especially attractive for compliance and brand perception.

This is already stimulating the evolution of paper packaging, and in particular formats that can deliver suitable barrier protection. Green alternatives under development within plastics include:

- Use of more recycled plastic content without compromising material performance

- Improving the recyclability of current packaging options with more monomaterial constructions

- Identifying suitable markets for flexible biopolymers.

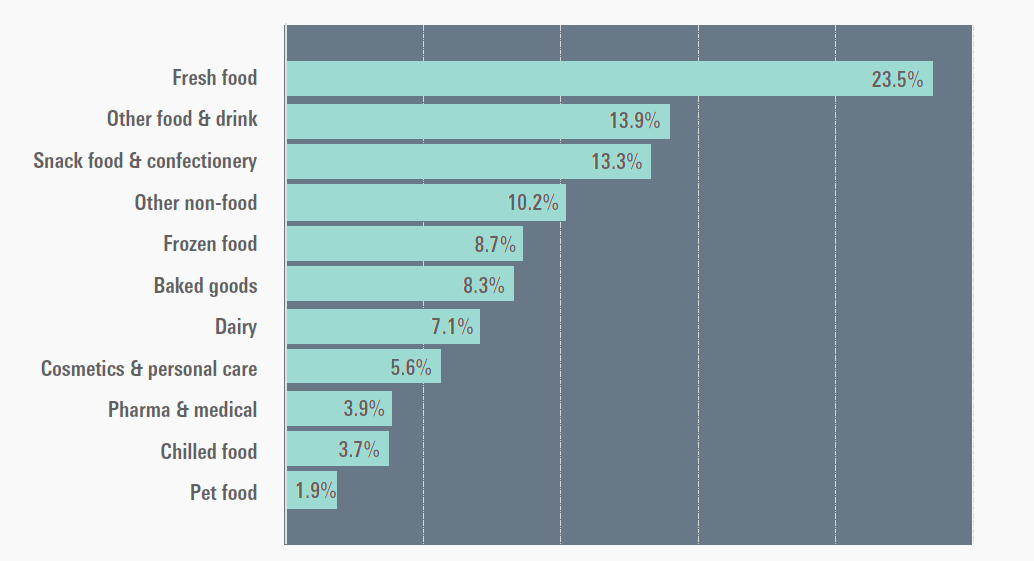

End-use applications

Food continues to be the largest end-use application for flexible packaging, representing 75.5% of overall use volume in 2021. The Covid pandemic has had a major impact on multiple areas, including the economics, productivity and ultimately demand in end-uses sectors; and the priorities of suppliers and brand owners.

Packaged food sales are far more resilient than other goods in periods of economic downturn. The nature of the Covid-19 pandemic with more consumers eating at home is – and will – continue to support this. The fastest growing end-use markets includes meat, fish and poultry and frozen foods with an average annual growth rate of 5.9% globally.

One segment that has been affected negatively is on-the-go flexible formats, though a degree of recovery will be seen as – and when – countries release their social distancing restrictions and hospitality venues reopen.

An emergent trend in the post-Covid world has been the use of at-home refill packaging for home and personal care products. This has generated new potential for flexible plastic refill pouches that minimise parcel size and shipping weight in transit.

Material use

Flexible papers represent only 8% of the world flexible packaging consumption in 2021, and moving forward over 90% of this market will be for polymer materials, including those used in multi-layer formats.

Polyethylene (PE) is the most widely used substrate by volume accounting for around 41% of the overall flexible packaging market; followed by biaxially oriented polypropylene (BOPP), and biaxially oriented polyethylene terephthalate (BOPET).

BOPP will be the fastest growing substrate over 2021-2026, with a forecast CAGR of over 5%. In contrast demand for regenerated cellulose fibre (RCF) and metal foil materials will increase only marginally across this period.