The desire for customized products is a significant driver for the adoption of digital textile printing, according to a new report from Smithers,

The Future of Digital Textile Printing to 2026. Over one-third of consumers are interested in personalized products that are commonly made with textiles, and individuals seeking personalization will pay a premium for these goods, Smithers’ research shows. Based on these drivers and other trends, digital textile printed volume will increase from 2021 to 2026 by 13.9% CAGR reaching 5.531 million square meters annually, data contained in the new report shows. Digital textile printed value will increase from 2021 to 2026 by 12.7% CAGR reaching €6.951 billion annually.

Digital textile printing continues to demonstrate strong growth opportunities for companies throughout the textile and printing supply chain. The global market for inkjet printing output on textiles rose in volume from 1.635 million square meters in 2016 to 3.160 million square meters in 2019. Valuation of digital textile printing also grew from €2.2 billion in 2016 to €4.1 billion in 2019. The global pandemic caused a hiccup, but overall growth of digital textile printing was strong at 11.9% CAGR by value from 2016 to 2021 and 12% by volume from 2016 to 2021.

The rebound from COVID-19

Digitally printed textiles performed better than the overall textile market during the pandemic. As consumers stayed home, fashion and signage declined most significantly. Home furnishings grew as consumers invested in refreshing their living spaces. Sails, a segment of the technical segment, also grew owing to an increased demand for outdoor water sports. The digital textile market will grow at a more rapid pace from 2021 to 2026 as the overall printed textile industry recovers from the global pandemic. Regionally, Asia will return to pre-pandemic levels first – by the end of 2021, followed by North America in 2022 and Western Europe and the rest of the world by the end of 2023.

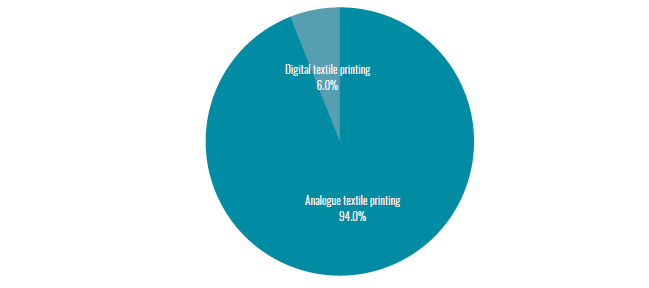

Market penetration

Digital textile printing has a global printed textile market penetration of about 6%. During the forecast period, penetration will reach 10%. This is low compared to other digital print applications such as commercial printing, ceramics or labels where penetration has been much higher. The lag in adoption is not because of a lack of demand. Rather, the technology and supply chains needed time to catch up. On trend with how most markets progress through the technology adoption curve from nascency to mainstream, growth rates will be high for digital textile printing given the low market penetration and will taper off as the base grows. Value growth rates will lag volume growth rates as pricing stabilizes with the benefits of a scaling market.

Global digitally printed textiles market penetration by volume (square meters)

Source: Smithers

End-use markets

Source: Smithers

End-use markets

Clothing has the highest market penetration for digital textile printing as it leverages ink advancements in digital dye printing, both dye sublimation and reactive. Signage is the next largest segment and also uses a significant amount of dye sublimation printing. Pigment printing is gaining traction in the space for backlit soft signage. The home furnishings section has also increased as consumer demand for refreshing the home has increased. Pigment printing is popular in the space for its light-fastness properties, but reactive printing is heavily utilized for its high color vibrancy and low costs. Technical textile digital printing remains nascent. This segment prioritizes functionality over design and color. Thereby, the technical textile segment will remain nascent throughout the forecast period.

Printing format

The majority of digital textile printing is done in a roll-to-roll process whereas a roll of textile is printed, then cut and sewn into the finished product. Scanning head machines dominate the space with thousands of installations versus an alternative method of high-speed, high-volume digital printing called single-pass, where printheads remain fixed in place and the substrate moves under the heads. The limited number (<50) of global installations of single-pass printers represents hundreds of millions of square meters of fabric printed annually. Both processes will grow during the forecast period. Direct-to garment printing makes up about 5% of market penetration on a volume basis. Here, garments and accessories are printed after they have been cut and sewn. The process continues its popularity in the US and Western Europe where consumer desire to pay a premium for custom products is on the rise coupled with a local textile supply chain that is lacking in sufficient cut and sew capability to enable scale.