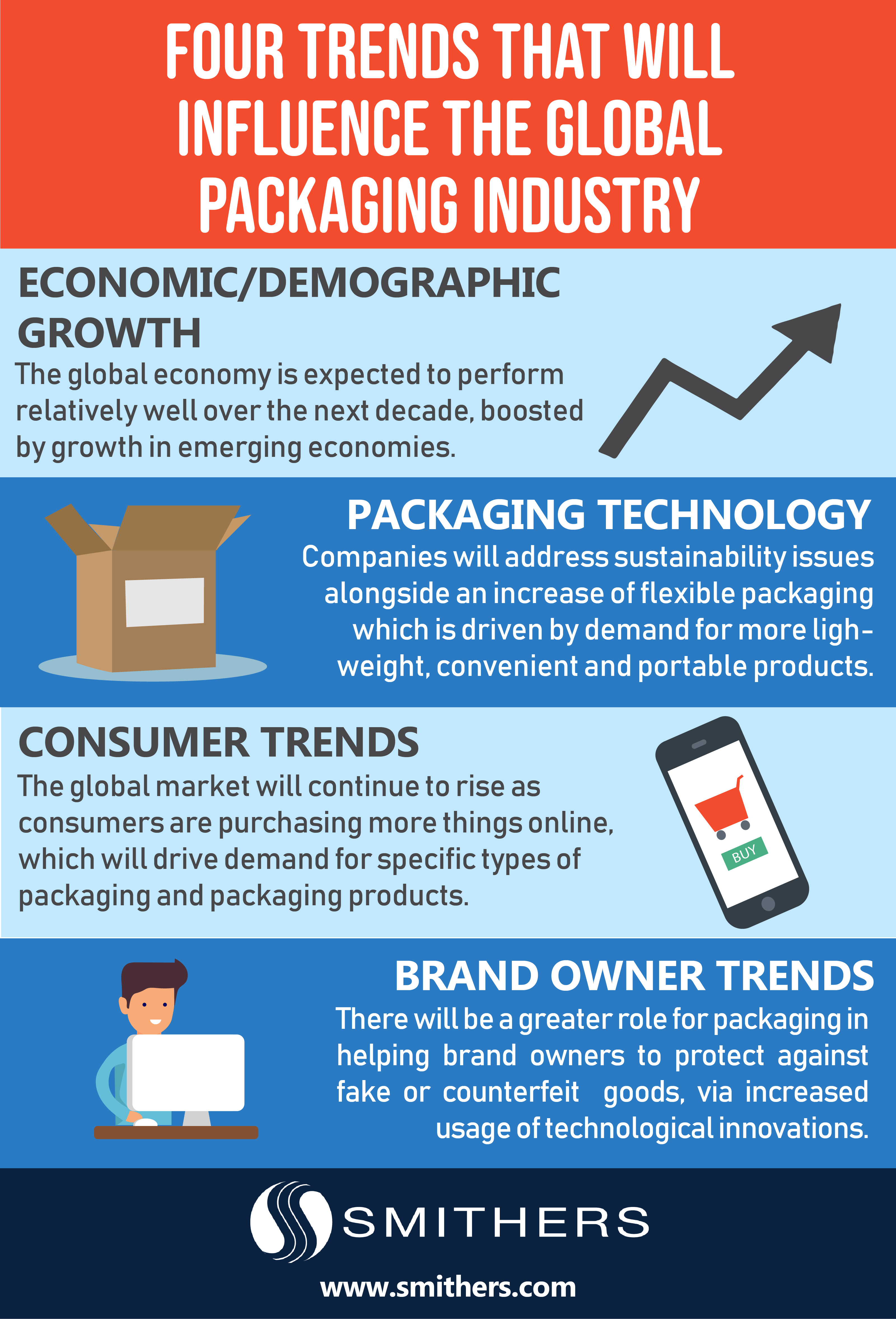

Market Report

The Future of Corrugated Packaging to 2029

The corrugated packaging market is growing quickly, helped by the explosion of e-commerce and developments in digital printing technologies.

The global corrugated packaging market is growing faster than expected, confounding some predictions that forecast a slowdown in corrugated consumption. A downturn in demand in China and the banning of contaminated recycled paper stocks has not fully materialised.

Smithers new report - The Future of Corrugated Packaging to 2023 - offers exclusive analysis on how this market is increasing, growing around 3.7% annually to reach $300 billion in 2023. The report also reveals that the electrical goods end-use sector will see the highest levels of growth.

E-commerce

E-commerce retail sales are continuing to rocket, with estimates of around 20% annual growth in e-commerce trade in Europe.

Global online sales are expected to be over $5.5 trillion in 2023. This will have a profound impact on packaging demand, especially in the corrugated industry as it represents 80% of demand in e-commerce.

The increasingly complex logistics chain for direct to consumer delivery – e-commerce packages are expected to be handled up to 20 times or more during standard distribution – means there is new demand for cost-effective secondary corrugated board packaging.

Demands from brand owners are now being felt by the converting industry as many brands now require the secondary pack to carry their image into the home, not just the retail outlet. This increases the need for converters to produce high-quality graphic designs on the shippers themselves.

Born out of e-commerce has been the advent of fit-to-product (FtP) or box-on-demand systems, driven in particular by the needs of dedicated e-commerce sellers such as Amazon and Staples. This technology enables the production of customised secondary packaging based on the exact size of the product being packed, including irregular shapes. For the end-user this eliminates the need for large inventories of standard-sized boxes which often require copious amounts of filler material.

As FtP platforms become more popular, there will be more demand for boards sold as fanfold, as well as finishing equipment, such as printers, that can operate with them.

Major moves are being undertaken to capitalise on this growth market. WestRock for example acquired Plymouth Packaging. Based in Michigan it derives 70% of its sales from its BoD systems and corrugated fanfold, together with its equity interest in Panotec and exclusive right to distribute Panotec’s equipment in the US and Canada.

Corrugated board is proving popular in packaging as sustainability becomes a more important issue across the value chain – it is easy to recycle and the pulp and paper industry is already adept at converting these into new generations of containerboard. These qualities mean there has been a rise in popularity of corrugated protective formats over polymer based alternatives, such as expanded polystyrene (EPS) foams.

While lightweighting of board has long been affecting the corrugated industry, rightweighting, and rightsizing are playing an increasingly important role in this market, not only in response to consumer demand for efficient packaging, but also in response to the logistics chain’s adoption of dimensional weight (DIM) pricing. In some instances substituting to a heavier board grade can have a beneficial impact overall as it allows for the elimination of additional protective elements,

The desire to minimise the volume of air being shipped within all delivery channels means that in some instances there have been significant cost increases. For example a 32-pack of toilet rolls costs an estimated 37% more to ship using charges based on dimensions, rather than simple weight.

Lightweighting has been particularly successful in Western Europe, where box weights are now typically about 80% of US weights. The importance of lightweighting will continue to be felt over the coming years as retailers look to save costs as well as appealing to end users.

Retail-ready packaging has established itself as a major cost saver for retailers, especially in Western Europe. This ongoing profit pressure is providing an impetus to use more retail ready formats as a labour-saving solution, as it is estimated that these secondary packaging formats can reduce shelf restocking and handling costs by up to 50%. It is also particularly popular with sales into convenience stores or discount retailers such as Aldi and Walmart. For brands it gives the added bonus of giving them greater control over the presentation of their goods within the retail space.

The expansion of e-commerce trade into the grocery sector is likely to have a slight impact on retail-ready packaging use as online sales do not require these pack types.

Corrugated cases will still be used to ship goods to an online retailers warehouse or ‘fulfilment centre’ but these do not need to be retail-ready formats. The emergence of subscription box and meal kit services – which offer direct-to-consumer delivery of specialist food using a weekly or monthly subscription – are providing some new opportunity for corrugated board suppliers with delivery-friendly formats containing goods within a die-cut interior.

As the digital print market matures, the corrugated sector, while still in its infancy, has developed a growing appetite for adoption of the process, and systems are now being developed to address the demands of the high-volume liner and post-print markets.

The flexibility of run-lengths, savings in set-up costs, the ability to personalise either relating to brands, regions, stores or individuals, and the level of quality now available through the latest technologies all combine to create a ‘perfect storm’ of growth opportunities for converters and printers.

Brand owners are recognising the opportunities to grow dwindling brand loyalty through greater engagement with their customer base provided by these technological developments, and industry leaders see packaging as an important component in the creation of a memorable shopping experience that users will want to share via social media, which can drive marketing, encourage repeat business and attract new customers.

The Future of Corrugated Packaging to 2023 offers comprehensive market data for current and future demand for corrugated packaging, complemented with over 350 tables and figures delivering an unparalleled level of detail across all key segments. Download the market report summary.